Avoid Pet Debt: Love Your Pets but Don’t Break the Bank

August 5, 2025

Debt Write-Off: What It Means for You

September 24, 2025

We’ve spoken a lot about the reciprocal link between mental health and money worries. Many of us face debt at some point in our lives. From unexpected bills to an unexpected or sudden change in circumstances, financial problems can happen fast – and to anyone. Regardless of the size of the debt or how it came about, money worries can feel overwhelming.

Does worrying about money keep you awake, or cause crushing feelings of dread? You’re far from alone. You’ll know all too well how it can affect your mood, your focus, your relationships and even your ability to cope with day-to-day stuff. We’re here to help you understand the link, the risks, and how to get better.

Does Debt Make Mental Health Worse?

But can debt actually cause mental health problems? Debt and money problems can certainly contribute to worsening mental wellness. At the same time, it’s important to remember that mental illness is complex. While money worries can be a major factor, some mental health conditions are rooted in biological or chemical imbalances in the brain and are not simply the result of life circumstances. However, if you’re already struggling with mental health concerns, money problems can make everything feel worse. And, if your mental wellbeing affects your ability to work, it becomes a difficult cycle to break.

So, yes, debt can impact your mental wellbeing, and mental illness can make debt harder to manage. Most importantly, we can advise you where to turn for help. Please know that help is available, there’s no judgment, and everything can get better.

The Debt and Mental Health Connection

The link between debt and mental health issues is undeniable. Research from the Money and Mental Health Policy Institute shows that:

- 46% of people in problem debt also have a mental health problem.

- People with mental health problems are three times more likely to be in problem debt.

So, the link works both ways: Debt leads to mental health challenges – stress, anxiety, and depression can develop or worsen when money is tight, and mental health challenges can lead to debt. Sadly, certain conditions make managing money harder, which can lead to arrears.

Arrears can build up and this creates a cycle: Debt leads to stress and anxiety, which can cause difficulty coping. When we’re struggling to cope, we’re likely to miss payments and thus incur even more debt. And so it continues… We can help you break that cycle.

How Debt Affects Mental Health

Debt affects mental health in three key ways. Firstly, there’s the emotional impact of being in debt. This includes:

- Constant worry and overthinking.

- Feelings of guilt, shame, or hopelessness.

- Reduced self-esteem.

There’s also a distinct physical impact which can worsen the emotional effects, and vice versa:

- Difficulty sleeping and insomnia.

- Tension headaches or muscle pain.

- Tummy problems.

- Fatigue from stress.

The emotional and physical impacts can then also add to the social impact, such as:

- Avoiding social situations due to cost.

- Withdrawing from friends or family.

- Strained relationships due to financial stress.

- Increasing isolation

All this can, you guessed it, create even more problems as talking to friends and family can be a tremendous help when you’re feeling down. That’s why we’re here to talk to.

When Mental Health Issues Come First

It’s vital to recognise that mental illness can, and does, occur independently of money problems. Conditions like depression, bipolar disorder, and schizophrenia have strong biological and neurological components. In these cases:

- Changes in the brain’s chemistry can affect mood, decision-making, and energy levels.

- Medication side effects, or the symptoms themselves, can make work and managing money more difficult.

- Periods of poor mental health can lead to missed payments or reduced income, which can then trigger debt.

In other words, debt may make an existing mental health condition worse, but it’s not always the root cause.

In these cases, you have certain rights:

Debt and Mental Health Evidence Form (DMHEF) allows your medical professional to confirm to creditors that you have a mental health condition affecting your finances.

Equality Act 2010: if your mental health condition counts as a disability, you may be entitled to reasonable adjustments from service providers and creditors.

How to Recognise the Warning Signs

If you’re struggling with money, it’s important to ask for help or advice. If you’re not sure where to turn, we can guide you in the right direction. If you’re feeling stressed, anxious, or overwhelmed, it’s vital to take stock and look after yourself. You may be experiencing debt-related mental health strain if you:

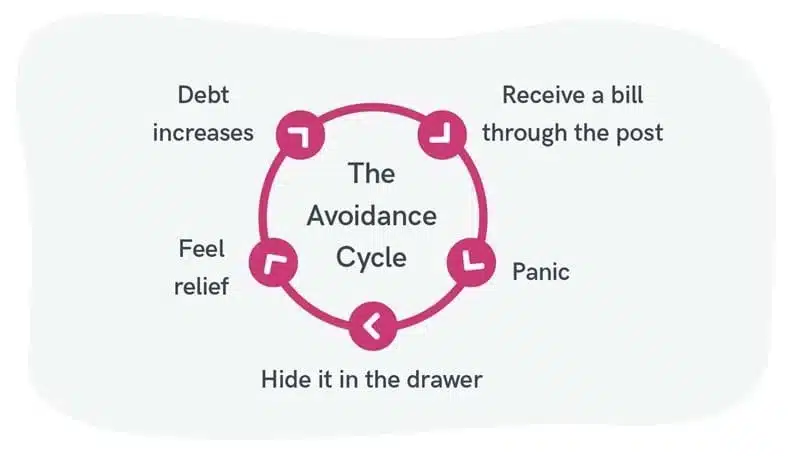

- Dread or avoid opening bills.

- Don’t check your bank account or open bank statements.

- Feel a sense of panic when thinking about money.

- Notice your mood changes around payday or payment deadlines.

- Can’t sleep due to financial thoughts running through your mind.

If you recognise any of these warning signs, please ask for help. If you don’t where to look or who to ask, contact us. Our Support Hub has links to countless organisations who can offer help, support or advice in most situations.

How to Break the Debt-Mental Health Cycle

You can break the cycle – but you may need help.

First, address the financial side. You can contact us in confidence and also seek free debt advice from charities such as StepChange, National Debtline, or Citizens Advice. Then, try to make a realistic budget, starting with essentials like food, rent or mortgage, and energy bills. If you’re in, or approaching, crisis, explore the Debt Respite Scheme (Breathing Space), which can pause interest and charges for 60 days (or longer for those in mental health crisis treatment).

To address the mental health side, you can take comfort from the fact you’ve taken steps to get back on track with money. It’s vital to speak to your GP about how you’ve been feeling so they can offer support or refer you to local NHS talking therapy services. Don’t be afraid to contact mental health charities like Mind or call Samaritans free on 116 123.

Just take baby steps and be kind to yourself: recognise even the smallest steps forward. Aim to build daily habits to support wellbeing: regular sleep, movement (don’t underestimate the power of a walk in the countryside or a local park), and social contact.

Moving On

Just as debt doesn’t define you, nor should your health concerns. Things can get better. Debt and mental illness can be a difficult mix, but with support, both your finances and your mental health can recover. Reaching out is the first and most important step.

Many of us have been where you are now – feeling trapped and unsure of the next step. With the right help, both debt and mental health can be managed. Whether it’s a payment plan, professional therapy, or simply having someone listen without judgment, there is a way forward.

Contact us and we’ll help you take that first step.