Mental Health and Money Matters

April 22, 2025

Secured and Unsecured Debts – What’s the Difference?

June 18, 2025

If you’ve ever applied for a mortgage, or to rent a property, or even just take out a new phone contract, chances are you’ve heard mention of ‘Credit Checks’ and ‘Credit Scores.’ Many of us know they exist – but what do they mean for us?

Understanding your credit score is vital for keeping on top of your creditworthiness and managing your financial health. Here’s a straightforward guide to help you get to grips with yours.

What is a Credit Score?

Your credit score is a number indicating your ability to repay any money you borrow – it represents how creditworthy you’re deemed to be. It’s intended to indicate how likely you are to repay any money you borrow, or to keep up repayments on a credit agreement – such as that new phone contract. All sorts of lenders use this score to assess the relative risk of lending to you. Each lender may use different criteria to evaluate your ability to pay.

The first credit score in the UK was introduced in the 1950s, though the basic concept of evaluating someone’s creditworthiness came earlier – as early as 1803, when London tailors shared information on debt defaults. More recently, the Consumer Credit Act of 1974 established a regulatory framework for the credit industry to ensure fair and responsible lending practices.

Is a Credit Score the Same as a Credit Report?

A credit report and a credit score are closely related, but refer to different things:

Credit Report:

A Credit Report is an in-depth record of your credit history, compiled by a Credit Reference Agency (CRA) like Experian, Equifax, or TransUnion. It includes:

- Your name, address, and date of birth

- Current and past credit accounts (credit cards, loans, mortgages)

- Payment history (including any missed or overdue payments)

- Public records (e.g. bankruptcies, CCJs)

- Electoral register information

- Record of any recent ‘hard searches’ (when a lender checks your file)

Lenders check your credit report to assess your ability to repay when you apply for loans, payment instalments and other credit.

Credit Score:

Your Credit Score is an overview of your credit report, given as a number.

- It’s a simplified measure of how risky you might be as a borrower.

- Each Credit Reference Agency calculates their credit scores differently (e.g. Experian’s scale is 0–999; Equifax uses 0–1000; TransUnion uses 0–710).

- A higher score generally means a better credit rating, but lenders don’t just rely on this score. Lenders will interpret your full report based on their specific criteria.

To simplify the difference, think of your credit report as a full structural survey on a house you’re looking to buy. Your credit score is more like a mortgage valuation, which gives little more than a number.

Who Holds Your Credit Information?

There are three main Credit Reference Agencies (CRAs) which compile and maintain your credit information:

- Experian

- Equifax

- TransUnion

The credit reference agencies collect data from various sources, including banks, utility companies, and public records such as the electoral register. This information is to create your credit report. Each agency may hold slightly different information about you, as not all lenders report to all three.

Check Your Credit Report

You can check your credit report for free with any of the three main Credit Reference Agencies (CRAs). Somewhat ironically, some of these agencies will offer and even promote a paid service. There’s no need to part with any money – you can see the information you need with no cost:

- Experian (UK’s largest CRA)

- Free Service: Experian Free Account

- What you get: Access to your credit report and score, updated monthly.

- Optional: They offer a paid “CreditExpert” service, but the basic version is sufficient for most people.

- Equifax

- Free Service via Clearscore: www.clearscore.com

- What you get: Access to your Equifax credit report and score, updated weekly.

- Note: You don’t need to sign up directly with Equifax unless you want a more detailed paid report.

- TransUnion

- Free Service via Credit Karma: www.creditkarma.co.uk

- What you get: TransUnion credit report and score, updated weekly.

- Includes personalised credit tips and loan offers.

Optional: Statutory Credit Reports

Legally, all Credit Reference Agencies have to provide you with a free statutory credit report. You can request it directly from:

- Experian Statutory Report

- Equifax Statutory Report

- TransUnion Statutory Report

These free versions are basic and don’t include a score, but they contain the essential information.

Does Debt Impact Your Credit Score?

Do existing debts and borrowing impact your credit score? Well, the answer is yes – but not always negatively. It’s all about how you manage your borrowing:

Potential Negative Impacts:

- High Credit Utilisation: If your credit cards are close to their limits, it signals risk. Ideally, try to use under 30% of your available credit.

- Multiple Hard Searches: Applying for a lot of new credit over a short time can cause temporary drops in your score due to hard inquiries.

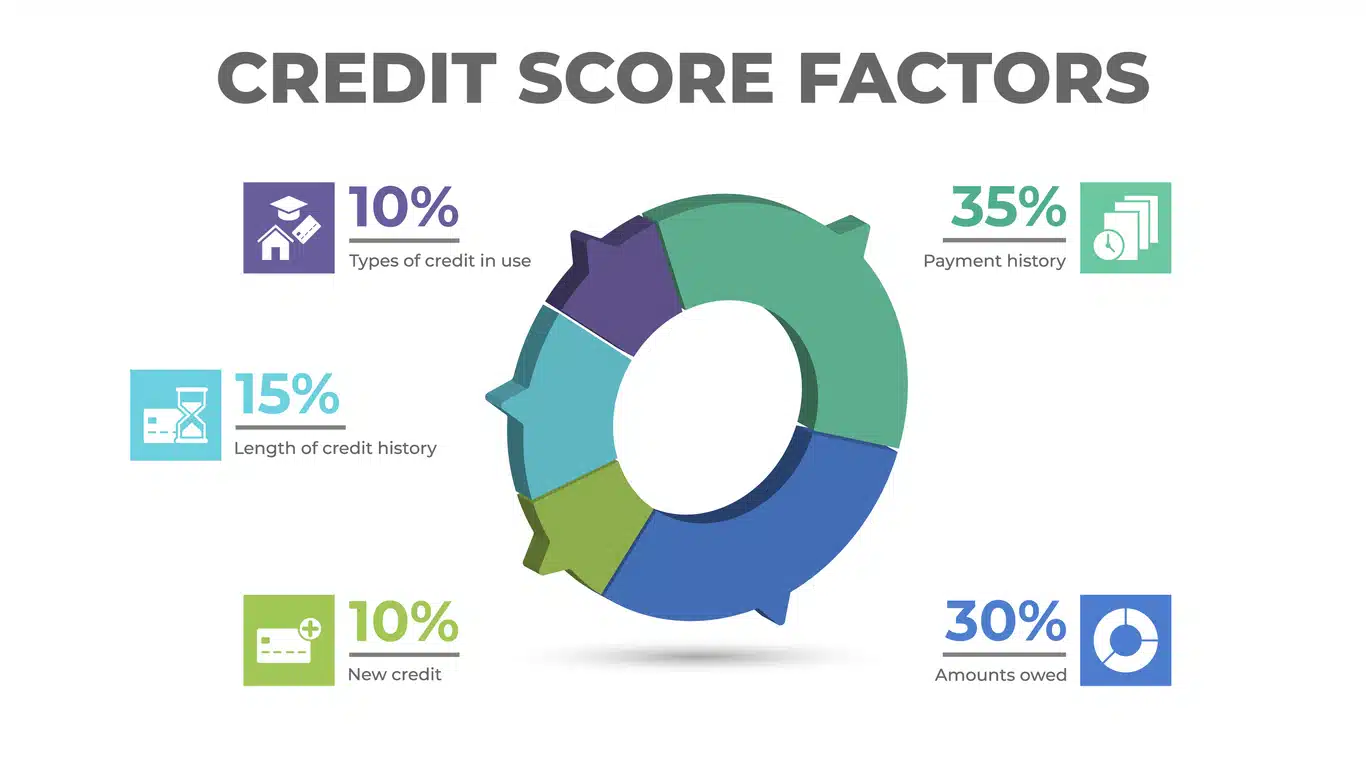

- Late or Missed Payments: Your payment history is probably the biggest factor in your credit score. Missing payments on any debt will severely harm your score.

- Too Many Accounts with Balances: Even when you always pay on time, having several accounts with outstanding balances can damage your score.

Potential Positive Impacts:

- Credit Mix: Having diverse types of debt (for example, a mortgage, car loan, and a credit card) can help your score by showing you can responsibly manage several types of credit.

- Paying On Time: when you consistently pay all debts on time, that strong history builds and sustains a healthy credit score.

- Established Credit History: Older accounts, even with balances, can positively contribute to your score if they show a long record of responsible use.

Having debts isn’t necessarily the end of the world for your credit score – how you handle them is key. Looked after well, they can give your number a boost. Always make payments on time, minimise balances, and don’t make too many new credit applications.

What Do the Numbers Mean?

Each Credit Reference Agency uses its own particular scoring system and lenders may interpret them differently based on their own specific criteria. Invariably, though, a higher score is desirable and taking steps to improve your score is always a good idea. It can be easier than you may think – and it’s well making the effort.

How to Improve Your Credit Score

Improving your credit score is all about demonstrating responsible financial behaviour. Such as:

- Pay Your Bills on Time: Consistently paying bills promptly shows reliability. If you can, set up direct debits to avoid missed or forgotten payments.

- Manage Your Credit Use: Avoid maxing out your credit cards. If possible, use less than 30% of your available credit limit.

- Limit New Credit Applications: Multiple applications over a short time can be a red flag and can negatively impact your score.

- Regularly Check Your Credit Report: Regularly review your credit reports and look for potential errors. You can inform agencies of debts that have been paid and dispute any inaccuracies.

- Be on the Electoral Register: Being registered can positively influence your credit score.

These steps can all help you to improve your credit score over time. Some things will show results quite quickly.

What Can Harm Your Credit Score?

Certain actions will almost certainly have a negative impact your credit score:

- Late Payments: A history of late and overdue payments can harm your creditworthiness.

- Missed Payments: Missing even one due payment can lower your score.

- High Credit Use: Using a substantial portion of your credit limit may signal financial distress.

- Frequent Credit Applications: Applying for multiple credit accounts in a short time can be seen as risky behaviour.

- Defaults and Bankruptcies: Serious financial issues will remain on your credit report for several years. This is why we need to be careful when dealing with problem debt – some solutions may not be the best option for everyone. That’s why we’ll always help find the best course of action for each individual.

Being aware of these factors, and taking care around debt and credit, can help you keep a healthy credit score.

Why Does Your Credit Score Matter?

Your credit score will make a significant difference to your ability to:

- Obtain Credit: Lenders use your score to decide whether to approve credit applications.

- Secure Favourable Interest Rates: A higher score can lead to lower interest rates on loans and credit cards.

- Rent a Property: Landlords usually undertake credit checks as part of the rental application process.

- Job Applications: Even employers sometimes check credit scores, particularly for finance roles.

Maintaining a good credit score can make an enormous difference when you need to borrow money, pay in instalments and even take out insurance policies or rent a house. Understanding and taking good care of your credit score is essential for your financial well-being – both now, and in the future. By keeping your eye on your score and taking the initiative to maintain or improve it, you can do yourself a real favour financially. And, these days, we could all do with one of those.